What 'Cap Rate Compression' Actually Means for Buyers in 2026

Cap rate compression is why you borrow at 6.5% and buy a 4% yield — negative leverage. What it means for your 2026 deal, and when cap rates decompress.

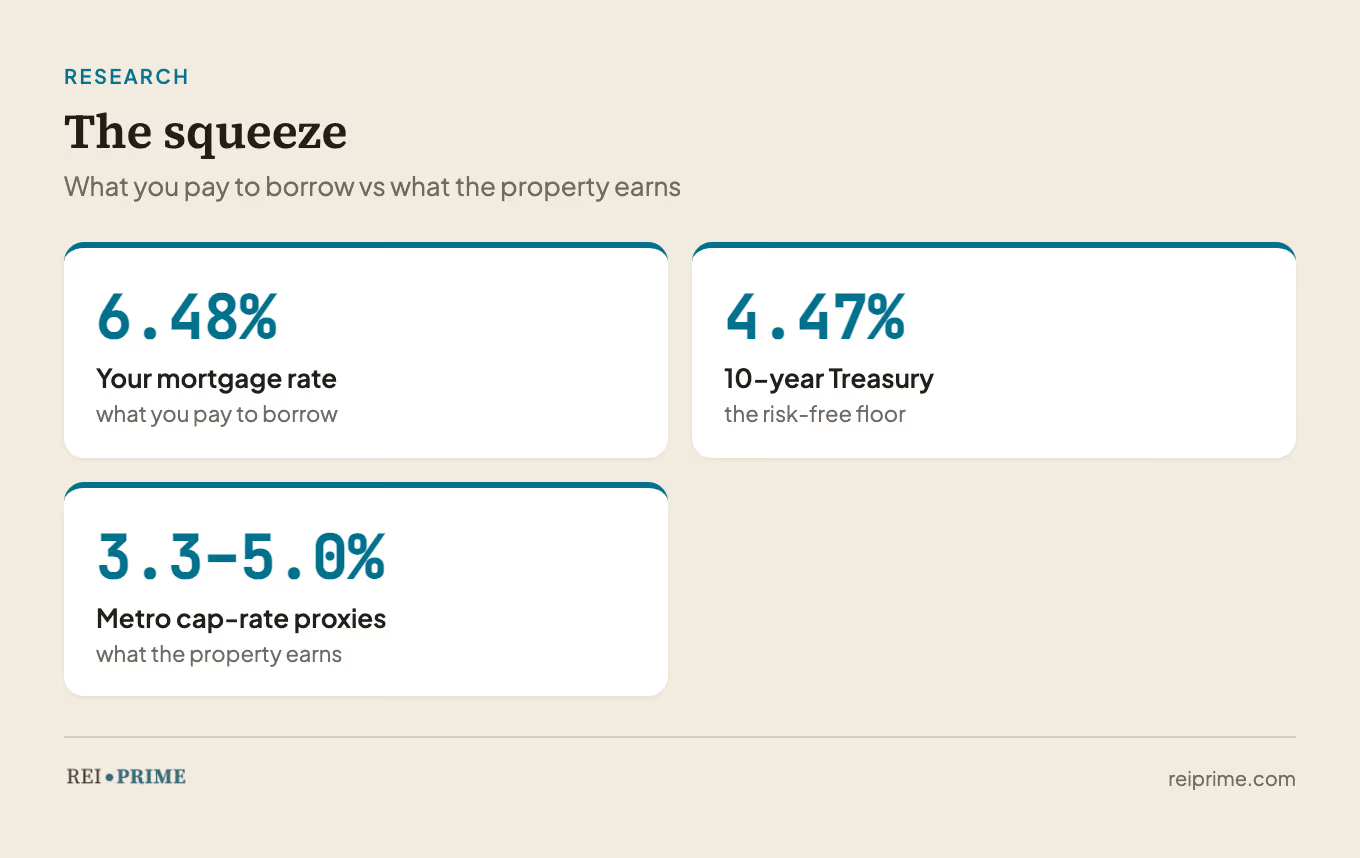

You can borrow money at about 6.5% right now and use it to buy a property that yields 4%. Read that again. You’d be paying more to rent the money than the building pays you to own it.

That gap — and the years of it baked into today’s prices — is what “cap rate compression“ actually means. Everyone uses the phrase. Almost nobody runs the number it implies. In 2026, it’s the most important math most buyers still skip.

What cap rate compression actually is

A cap rate is simple: a property’s net operating income divided by its price. A building throwing off $20,000 of NOI at a $400,000 price is a 5% cap. Move the price to $500,000 on the same income and the cap compresses to 4%. The yield fell. You’re paying more for each dollar of NOI.

That’s compression: cap rates falling because prices climbed faster than income. And it didn’t happen by accident. For most of the last decade, money was nearly free — when the safe alternatives pay almost nothing, investors bid real estate prices up until the yield is thin, because thin still beat zero. A 4% cap looked great next to a 1% Treasury.

Then rates moved. The safe alternative isn’t 1% anymore — it’s 4.47% on a 10-year Treasury and 6.48% on the mortgage you’d actually borrow. But prices, and the cap rates they imply, never fully caught up. The compression is still in there.

Why it bites in 2026: negative leverage

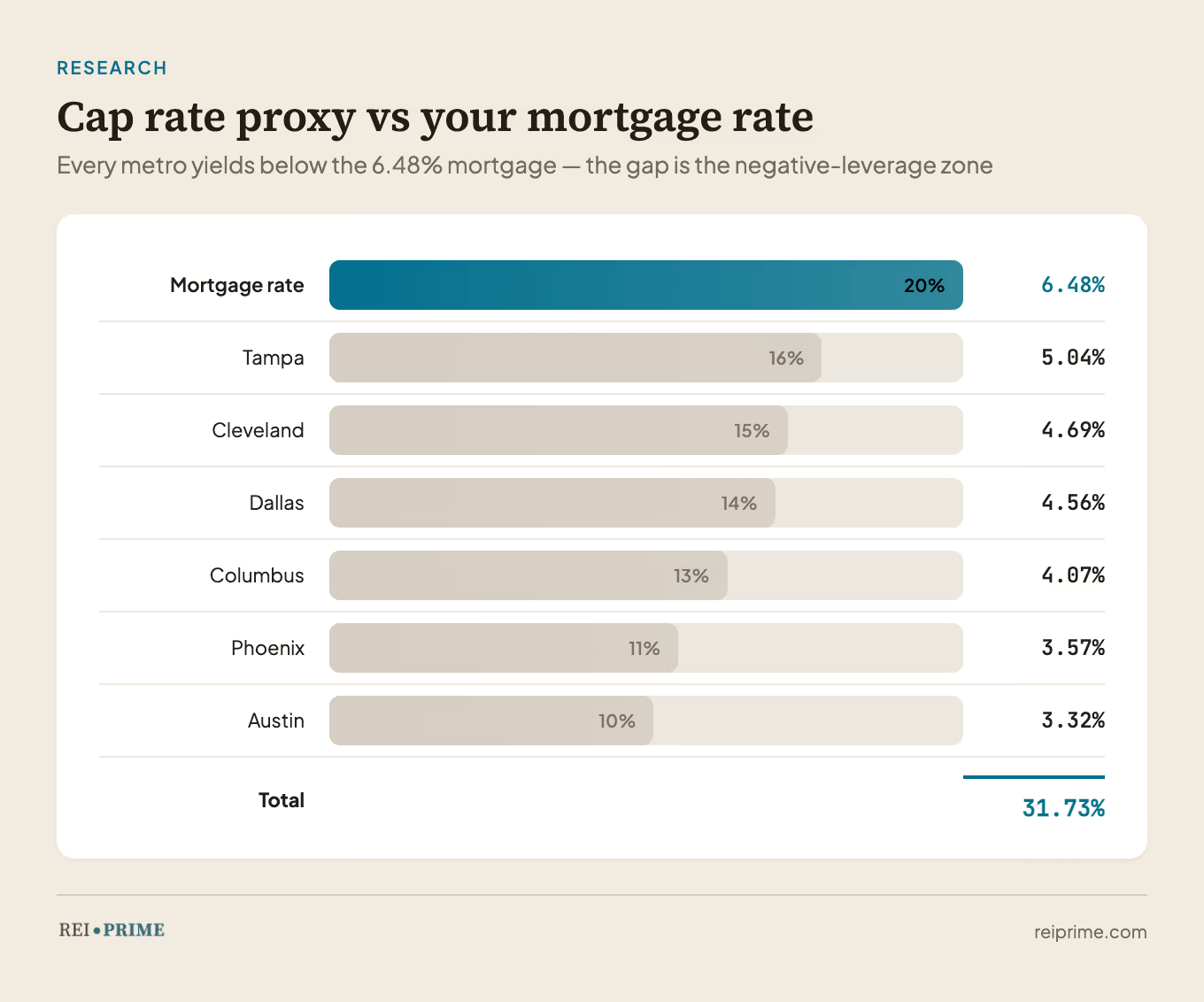

Here’s where it stops being academic. Look at what our own metro data shows for the cap rate proxy — NOI over price at the metro level:

Austin: 3.32%. Phoenix: 3.57%. The Sun Belt’s hottest metros are the most compressed.

Columbus: 4.07%. Dallas: 4.56%. Cleveland: 4.69%. Tampa: 5.04%. The value metros yield more.

Now put the mortgage rate next to those. At 6.48%, buying a 3.32% Austin cap means you’re borrowing at nearly double the property’s unlevered yield. That’s negative leverage: the debt drags your return down instead of lifting it. The whole point of a mortgage is supposed to be positive leverage — borrow below the cap rate, and leverage amplifies your return. Flip it, and every dollar of debt you add makes the deal worse.

In a 3.3% metro at a 6.5% rate, leverage is working against you. In a 5% metro, the math is tight but at least closer to even. That’s the practical difference between a “tight” cap and a “deal-by-deal” cap — and it’s why the same buyer gets a very different answer in Austin than in Cleveland.

To be fair, a compressed cap isn’t automatically a bad deal. A 3.3% going-in yield in Austin is a bet — that rents and prices grow fast enough to outrun the negative leverage — and sometimes that bet pays. The point isn’t that low caps never work. It’s that you’re underwriting growth, not income, and you’d better know which one you’re actually being paid for before you sign.

There’s a sharper version of this the pros lean on: the number that has to clear isn’t always the going-in cap. On a value-add — or a building you’re buying below replacement cost — what matters is the stabilized yield, the cap after you’ve brought rents to market or cut the expense load. Negative going-in leverage is a defensible entry toll when the path to that clearing stabilized yield is underwritten and real. It’s a trap only when nothing about the income is going to change.

The thinnest spread in decades

There’s a second comparison that’s even more sobering. Forget the mortgage for a second and just put the cap rate next to the risk-free Treasury — that’s your yield spread, the extra return you demand for taking real estate risk over a government bond.

A ~4% cap against a 4.47% 10-year Treasury is a negative spread on our metro proxies. You’d be accepting less yield than Treasuries to take on tenants, turnover, a roof that fails, and an insurance bill that keeps climbing. Zoom out to the broad institutional cap-rate series and the cushion is still positive — but only around 170 basis points — about 1.7 percentage points — near its tightest in 60 years and among the thinnest readings on record. Slice it either way — our residential proxy or the institutional series — and the premium that’s supposed to pay you for taking real estate risk is about as thin as it has ever been.

That doesn’t mean nothing pencils. It means the margin for error is gone. When the spread was wide, a mediocre deal still cleared. With the spread this thin, the deal has to be right — the cap has to genuinely beat your cost of capital, not “almost.”

So when do cap rates decompress?

This is the question every buyer is quietly betting on: rates are high, so cap rates should rise — decompress — and prices should fall to restore the spread. Buy now, the logic goes, and ride the re-rate.

Be careful with that bet. Cap rates are sticky, and they decompress slowly — through time, not a crash. The closest cycle parallel is the early 1990s: after a rate shock, NOI drifted roughly sideways for years while the market re-priced in slow motion, because sellers anchor hard to the price they “should” get and simply refuse to mark down. Inventory sits. Deals don’t trade. The spread normalizes, but it can take years — and you can’t underwrite a year of negative carry on the promise of a reset that arrives on nobody’s schedule.

A real signal that the re-rate is underway is in the supply data, not the price data — which is exactly what we read on EP 140, where builder margins compressed across the board first. Watch the pipeline, not the wish.

And watch the right number, because price drops show up last. A seller will let a listing sit for a year before cutting the sticker. The earlier tells are days-on-market stretching out, concessions getting deeper, and the supply pipeline drying up — the builder-margin signal that flagged the turn before a single price tag moved.

What a buyer actually does

You don’t fix compression by waiting for it to reverse. You out-position it. Three moves:

Buy a cap rate that beats your cost of capital. Hunt the higher-yield metros and counties where the cap genuinely clears your debt — a Cleveland or a Tampa, a value county — instead of paying a 3.3% appreciation bet in Austin. Our metro hubs show the cap-rate proxy for every market; start where the number works.

Force the cap up yourself. Compression is a market-wide phenomenon, but your cap rate is a building-level number. Raise NOI — under-market rents brought to market, an expense line cut, a unit repositioned — and you decompress your own deal on your own timeline. Where there’s genuine slack to capture, a building bought at a 4% cap that you push to a 5.5% effective yield through rents and expenses has decompressed for you — without waiting on the market, the Fed, or a single seller to capitulate. That lift isn’t automatic, though: it takes real below-market rent or operational fat to cut, so underwrite the slack honestly before you pay for it. That’s the one re-rate you control.

Set a floor. Pick a minimum cap rate above your market-normal plus a cushion, and a compressed metro screens itself out before you fall for the story. (It’s the same discipline behind the cap-rate floors we’ve used on the buy side — demand the cushion, in writing, before you tour.)

The number to run is the simplest one in the whole business: does this cap rate beat what my money costs? Plug your NOI, price, and rate into the calculator and look at the levered return. If the debt is dragging it down, you’re not buying a deal — you’re buying compression, and hoping someone else un-compresses it for you.

Cap rate compression isn’t a headline to fear. It’s a filter. It tells you, market by market, where your money is being paid to take risk — and where it’s being asked to take risk for free. Run it on every market you’re weighing: the metros where the cap rate clears your borrowing cost are where leverage still works for you; the ones where it doesn’t are where you pay cash, force the NOI, or walk. None of that requires predicting the Fed — it just requires running the one ratio most buyers skip. In 2026, the buyers who win are the ones who can tell the difference before they sign.